I wrote an article about power of compounding in May 2008, now i m revisiting this again. Why ?

Just a few weeks ago I came across one of Anthony robbin youtube video -

Once again the AMAZING magic of compounding, here's the example mentioned in the video. Next time, a guy come up to you and offer to bet on the golf holes with $0.10 and double up , tell him, "I watch the same video too" =D

Initially it really really slow but once it reach the 15th hole, the money start to explode exponentially!

From a $0.10 cents bet it can snowball to $13,100

In order to achieve the above, we will need to leverage on instrument or vehicle that can give us an annualized rate of return of 100% , lets see what are the commons instrument that give us ROI:

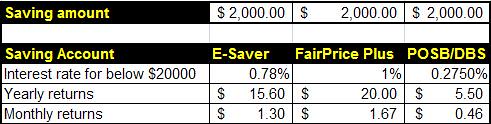

- Most basic, bank saving - (I wrote a few articles on this. One of it comparing interest rate offer by standard Chartered, fairprice plus and dbs - http://shulouto.blogspot.com/2008/05/highest-interest-rates-of-singapore.html) Just did a quite check, dbs saving account interest dip again to 0.125% pa; fairpriceplus dip to 0.200% pa; e$aver from standard chartered dip to 0.15% pa (man i miss those days where they offer 1.88% pa, i got like free movie tickets every month just only interest rate =D)

- Fixed deposit - posb offer 0.600% pa for 24 mth tenure and uob offer 0.700% pa for 24 mth tenure

- Investment link plan -5% (not guarantee)

- Index ETF ie Dow Jones or STI ETF (7 % average rate of return without dividend - base on http://bullythebear.blogspot.com/2008/05/thoughts-about-sti.html)

Scenario 1

An Exchange Traded Fund (ETF)

An Exchange Traded Fund (ETF)

Expense Ratio: 0.09%

Initial Investment: $10,000

Annual Rate of Return: 10% (Before Expenses)

Annual Rate of Return: 9.01% (After Expenses)

Time Horizon: 30 Years

Future Value: $133,042.43

Initial Investment: $10,000

Annual Rate of Return: 10% (Before Expenses)

Annual Rate of Return: 9.01% (After Expenses)

Time Horizon: 30 Years

Future Value: $133,042.43

Scenario 2

Average Actively Managed Mutual Fund

Average Actively Managed Mutual Fund

Expense Ratio: 1.50%

Initial Investment: $10,000

Annual Rate of Return: 10% (Before Expenses)

Annual Rate of Return: 8.35% (After Expenses)

Time Horizon: 30 Years

Future Value: $110,883.63

Initial Investment: $10,000

Annual Rate of Return: 10% (Before Expenses)

Annual Rate of Return: 8.35% (After Expenses)

Time Horizon: 30 Years

Future Value: $110,883.63

That's a 19.9% difference in your retirement, or in this case, $22,158.80...!

STI ETF was offer in April 2002

What's STI ETF - BACKGROUND

streetTRACKS STI, Singapore’s first locally created exchange traded fund, is designed to track the performance of the Straits Times Index (STI). Shares of streetTRACKS STI were listed and traded on SGX-ST since 17 April 2002.The Fund's investment objective is to replicate as closely as possible, before expenses, the performance of the Straits Times Index. There can be no assurance that the Fund will achieve its investment objective. The Fund will seek to achieve this objective by investing all, or substantially all, of its assets in Index Shares in substantially the same weightings as reflected in the Straits Times Index. Within the limits set out in the CPF Investment Guidelines, the Fund may invest in futures and derivatives instruments traded on Recognised Stock Exchanges and OTC Markets provided that such instruments are Authorised Investments.

The Manager employs an "indexing" approach intended to replicate as closely as possible the performance, before expenses, of the Straits Times Index. The Straits Times Index is a widely quoted indicator of the performance of the Singapore stock market. It currently comprises 50 common stocks which are selected by Singapore Press Holdings Ltd based upon certain market capitalisation and liquidity characteristics.

streetTRACKS Straits Times Index Fund has changed its name to SPDR Straits Times Index ETF with effect from 31 March 2011.

Here's the Strait Time Index (MAX chart)

This a recent performance of STI ETF from Jun 2009 to current.

Indices on a long run 10 - 20 years usually trend up, and for STI its a performance indicator of Singapore top 30 stocks ie, City Development, Capitaland, ComfortDelGro, SIA, DBS, starhub, NOL, Singtel, UOB, SPH, Semb Corp, OCBC, SMRT, ST Engineering - man for them to fail ? Definitely NO WAY! (This is strictly my personal opinion)

A level 1 person, either invest a lum sum or averaging the cost monthly into the STI ETF and pay the brokerage fee consistently and let it roll for many many years.

A level 2 person, sell when it's trending down and buy again when it's trending up - follow the wave

How to invest into STI ETF ? stay tune =D .......

Research :

http://www.moneytalk.sg/2008/11/why-invest-in-sti-etf.html

http://sg.finance.yahoo.com/q/cp?s=^STI